The 2026 Home Services Field Guide: 8 Forces Quietly Rewriting Who Wins

If you run a home services company in 2026, you're operating in the most lucrative — and most violently restructuring — version of this industry that's ever existed. The U.S. home services market is sitting between $650B and $750B annually. Demand is durable. In some trades, margins are the best they've ever been. And yet a lot of owners we talk to feel like the ground is moving under them.

It is.

What follows isn't a list of buzzwords or "tips to optimize your Google Business Profile." It's eight specific, well-documented shifts reshaping how money, leads, labor, and ownership flow through this industry — and what each one means for the operator who has to make payroll on Friday. The research behind this is pulled from PE deal trackers, SEC filings, BLS data, Google's own product documentation, the 2026 State of the Trades survey of 1,000+ contractors, Scorpion's 2026 survey of 2,000 homeowners, Whitespark's Q2 2026 local data set, and a stack of primary platform research most owners will never have time to read.

Read it through once. There's a payoff at the end.

In this guide

- Private equity isn't coming. It already came.

- The skilled labor shortage is a margin problem in disguise

- AI voice and SMS follow-up: from experiment to table stakes

- Google search just changed under you

- Google LSAs got harder, more expensive, structurally different

- Reddit, CTV, and addressable geofencing

- Recurring revenue is now a multiple-expansion lever

- Consumer trust has fragmented across platforms

- So what does this all add up to?

- A note on who wrote this — and why

1. Private equity isn't coming. It already came. And it's the single biggest force in your market right now.

Let's start with the shift that's restructuring the industry beneath everyone's feet.

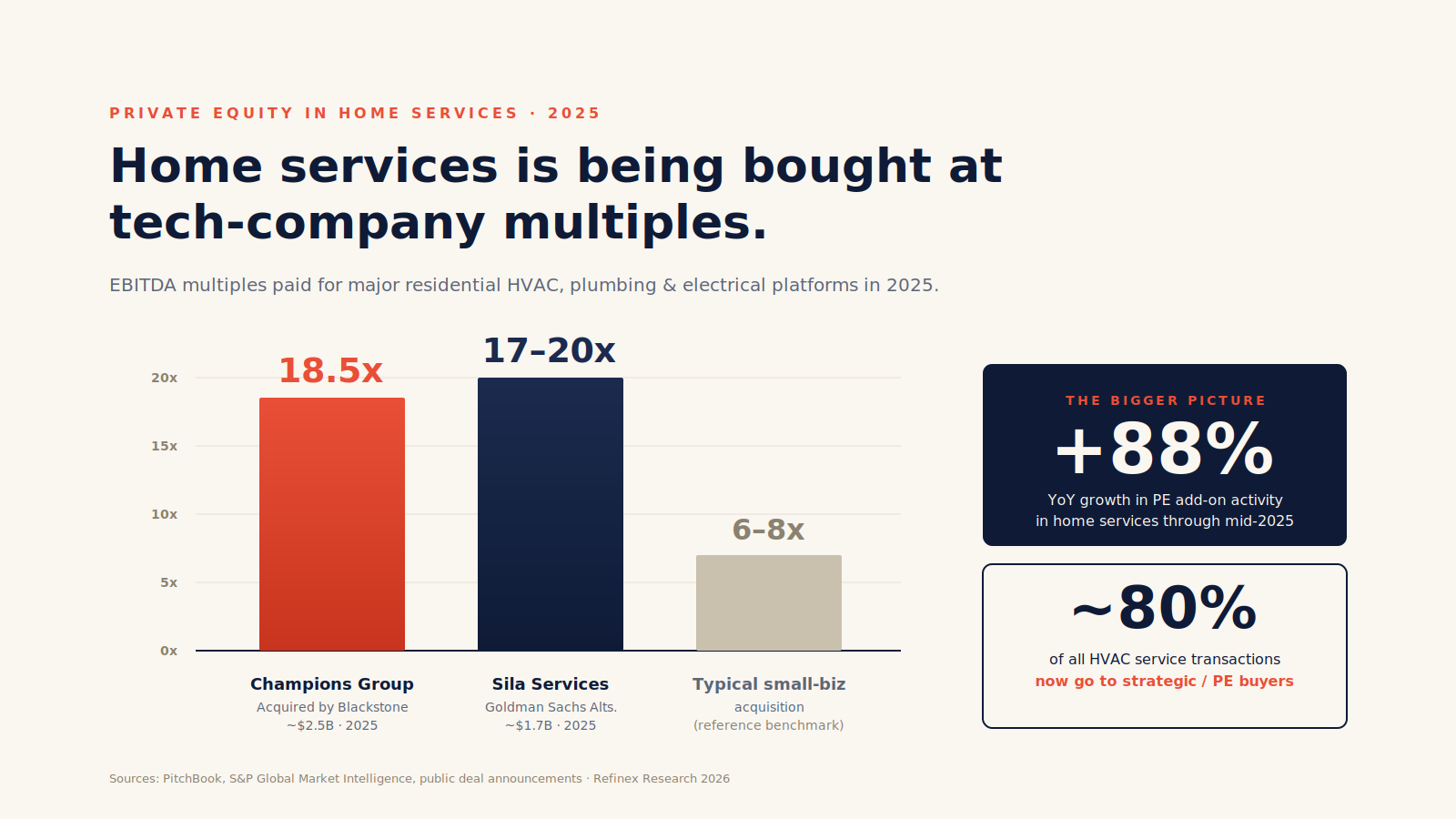

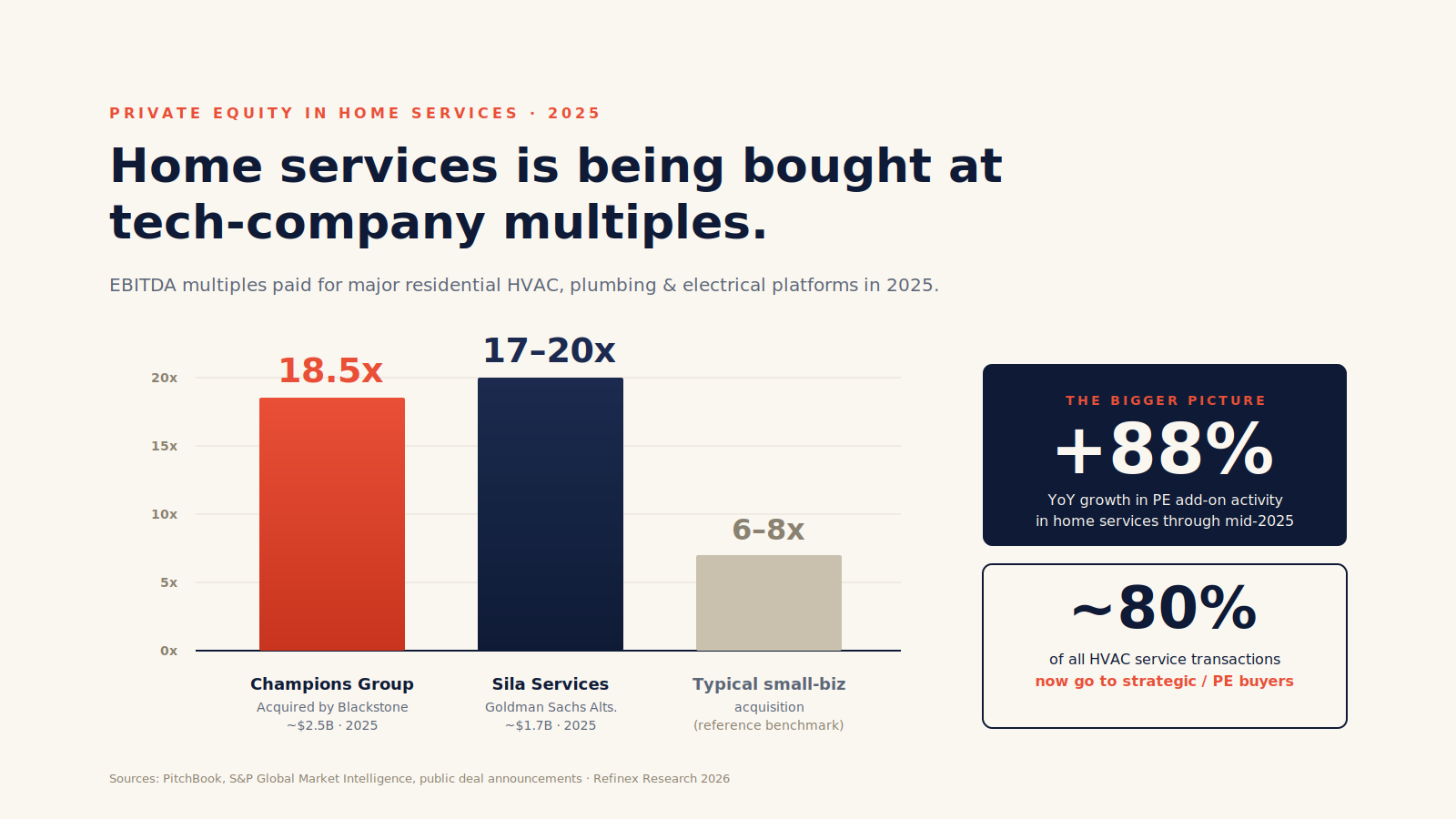

In 2025, Blackstone agreed to pay roughly $2.5 billion for Champions Group, a residential HVAC, plumbing, and electrical platform — at an implied multiple of around 18.5x EBITDA. A few months earlier, Goldman Sachs Alternatives took a majority stake in Sila Services at a reported $1.7 billion valuation, in the 17–20x range. Apex Service Partners alone closed roughly 60 add-on acquisitions in 2025 — more than the entire publicly tracked plumbing roll-up cohort combined.

The numbers behind the headlines:

- PE add-on activity in home services rose 88% year-over-year through mid-2025

- Strategic buyers now account for ~80% of all HVAC service transactions

- At least 27 active PE-backed platforms are competing for the same fragmented owner pool, with over $50B+ in committed capital

- Apex alone has raised over $6 billion in funding, including a $3.4B continuation fund — a structural signal that this is a multi-decade hold, not a 3–5 year flip

This is not a fad. It is a permanent restructuring of the competitive landscape. And it matters whether you want to sell or not.

Why this affects you even if you'd never sell in a million years:

When a PE-backed platform buys a competitor in your service area, three things happen within 12 months. First, they centralize back-office, get supply-house discounts you can't match, and squeeze 4–6 points of margin out of operations. Second, they raise technician pay — Alpine Investors reports a 20% average technician pay bump in year one post-acquisition — which pulls your best people. Third, they deploy a marketing budget calibrated against a portfolio of brands, not a single P&L, and they can run at a loss on lead acquisition in your market for 18 months to take share.

A huge tell most owners miss: many of these PE-owned shops keep the same local name, same family-feel branding, same logo after acquisition. The neighborhood doesn't know anything changed. But behind the scenes, the cost structure, the marketing budget, and the playbook just got an enterprise upgrade.

The strategic takeaway: The independent operator who isn't actively countering this is, quietly, losing a race they don't know they're running. The counter-move isn't to outspend them. It's to out-precision them: own a tighter ICP, run faster speed-to-lead, build channels they can't bolt on with a checkbook.

2. The skilled labor shortage isn't a hiring problem. It's a margin problem in disguise.

Every owner reading this already knows the labor side of the story:

- The U.S. construction industry is short ~530,000 workers in 2026

- For every 3 tradespeople retiring, only 1 new worker enters the field (NCCER)

- Projected 2026 shortages: 20,000+ licensed plumbers and nearly 40,000 HVAC technicians in the U.S. alone

- Median age of plumbers and HVAC techs now exceeds 40

Here's the part most operators are still underestimating: the labor shortage isn't your biggest bottleneck. Your back office is.

The single most consistent insight from operators running $5M–$50M shops right now is that field talent is half the battle. The other half — dispatch, intake, follow-up, estimate-to-close, scheduling, billing — is where deals die quietly. You can hire two more techs. But if they sit idle because intake isn't converting, or because nobody followed up on the 47 leads from last month, the new hires don't fix anything.

The math is brutal and worth sitting with:

A 2-tech shop missing 2 booked jobs per week at a $500 average ticket loses $52,000 a year. A 6-tech shop missing 8 booked jobs per week at $1,200 average ticket loses ~$500,000 a year.

Most owners don't measure this because the missed jobs never enter a CRM. They were a missed call, a slow text-back, a quote that didn't get followed up on day 3.

The strategic takeaway: The winning operators in 2026 aren't the ones with the most techs. They're the ones whose office-side conversion is engineered as carefully as their field operations. Speed-to-lead, follow-up cadence, and intake quality are now the highest-leverage margin levers in this industry — and most owners are still under-investing in them by an order of magnitude.

3. AI voice and SMS follow-up moved from "experiment" to "table stakes" in 18 months. Quietly.

You've heard the noise about AI. Strip away the hype and look at what's actually shipping into production at well-run shops.

The behavioral data that matters:

- Up to 78% of leads go to the first business that responds (HBR's foundational research on speed-to-lead, now widely confirmed)

- A lead responded to in 5 minutes vs. 30 minutes is 21x more likely to qualify

- The shared-lead platforms most contractors complain about (you know the names) sell the same homeowner to 3–5 contractors. First responder wins. Everyone else paid for nothing.

- Nearly 60% of homeowners who call after-hours and don't get a live answer will not call back

- HVAC contractors deploying always-on AI voice routinely report 40–50% increases in booked appointments from after-hours alone

In 2024, voice AI in home services was a curiosity. In Q1 2026, it is a settled question. A 2026 industry survey of contractors found about 25% are using AI meaningfully today — meaning roughly three-quarters of the market hasn't adopted yet. That gap is the opportunity. By the time penetration crosses 50%, voice AI stops being an advantage and starts being table stakes. Industry analysts project that crossover happens by end of 2026.

What good AI implementation actually looks like in this trade (not the demo-ware version):

- Inbound voice agents that answer in two rings, qualify on the call, hand off urgency to a human, and write the appointment into the calendar — not "press 1 for service"

- Outbound speed-to-lead that calls a web lead within 60 seconds of submission, before the homeowner has even closed the tab

- SMS follow-up sequences that pursue the 40% of leads who said "let me think about it" — most shops abandon these by day 2; a disciplined sequence over 14 days recovers a measurable share

- Multilingual handling — Spanish-speaking callers handled natively, no transfer drop-off

The catch most owners miss: voice AI is only as good as the systems plumbing behind it. If the AI books an appointment but doesn't sync to your dispatch, doesn't tag the lead source, doesn't enrich the contact with property data, doesn't trigger a follow-up if the homeowner ghosts — you've bought a fancy answering service. The competitive edge is in the integration, not the voice model.

The strategic takeaway: Speed-to-lead under 60 seconds, 24/7, with intelligent qualification, is the single largest lift available to most home services operators right now. It's also the single biggest gap between the top quartile and everyone else. The shops that lock this down in 2026 will be impossible to compete with on lead economics in 2027.

4. Google search just changed under you — and most contractors haven't noticed yet.

This one is the silent killer of 2026, and it's the trend that's least talked about because most contractors don't read SEO research.

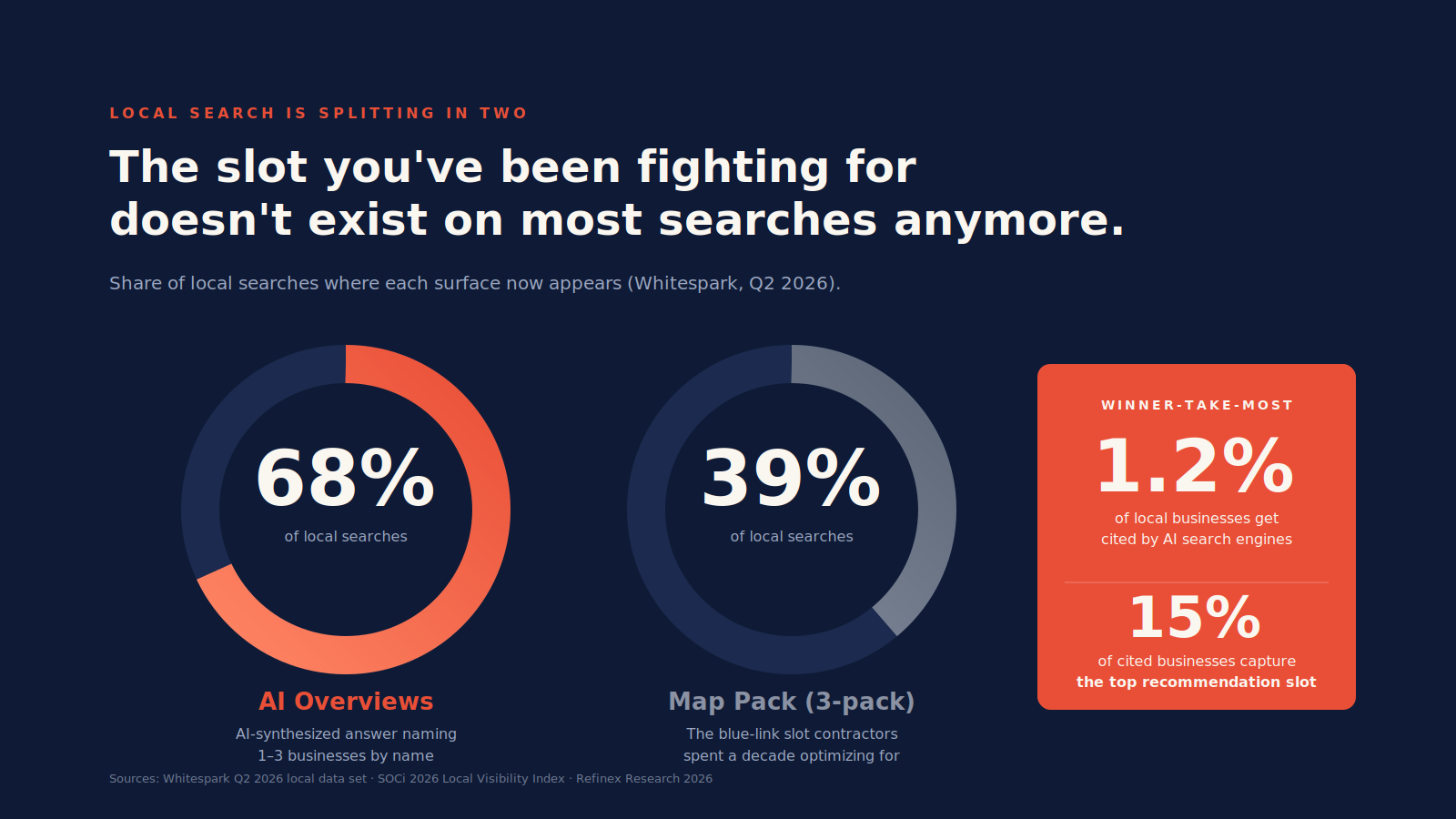

A 2026 local SEO data set found that AI Overviews now appear on 68% of local searches, 92% of informational local queries, and 97% of hybrid-intent queries like "average cost of HVAC replacement in Calgary." Map packs — the three-pack contractors fought for in the 2010s — now only appear on 39% of local searches.

Translate that:

The spot at the top of Google that you've been competing for, with your reviews and your GBP, no longer exists on most of the searches your customers are running.

What replaced it is a synthesized AI answer that names one to three businesses in your metro by name. Across all local business listings, only about 1.2% get cited by AI search engines (SOCi 2026 Local Visibility Index). For local services categories, only 15% of cited businesses capture the top recommendation slot where the actual conversion happens.

And the consumer behavior shift driving this is happening faster than most owners realize:

- 41% of consumers now trust AI recommendations for local services "as much or more" than personal referrals — up from 12% in 2024

- 1 in 3 homeowners under 45 have used an AI assistant to find a home service provider in the past 90 days

- AI-referred leads convert at substantially higher rates than Google organic leads because the homeowner already trusts the AI's recommendation before the call

This isn't theoretical. It's already how a meaningful slice of your customer base is finding their next contractor. And the contractors who get cited now will compound that authority: every AI-referred customer leaves a review, the review strengthens the trust signal, the AI cites them more often. The map-pack winner-take-most dynamic of the 2010s is repeating itself in AI search, and the lock-in is happening through 2026.

What actually moves the needle on AI citation (different from traditional SEO):

- Multi-source consensus — your business mentioned consistently across GBP, niche directories, forums (Reddit included), local news, industry publications — not just on your own site

- Structured data done correctly — proper LocalBusiness, Service, and FAQ schema. Sites with FAQ schema are 2.8x more likely to be cited in AI answers (FogLift 2026 study).

- Content that directly answers high-intent questions — "how do I know if my furnace is failing," "what does a tankless install cost in [city]," "how long do heat pumps last" — written like a tradesperson actually answers them, not like an SEO content mill

- Freshness — pages not refreshed quarterly are 3x more likely to lose AI citations than recently updated pages (AirOps research)

- Review velocity, not just volume — recent reviews matter more than historical totals

The strategic takeaway: If your entire local search strategy is "rank in the map pack and run LSAs," you are optimizing for a surface area that is shrinking every month. The contractors who own the AI citation in their metro by mid-2026 will own the recommendation slot through 2028, the same way map-pack winners owned the 2010s. Most of your competitors are still asleep on this. That's the window.

5. Google Local Service Ads got harder, more expensive, and structurally different — and the playbook from 2023 is actively losing money in 2026.

LSAs are still one of the highest-ROI channels in home services. They're also a very different product than they were 18 months ago, and a lot of owners are running them on autopilot with last year's strategy.

The structural changes you need to know:

- The old "Report a Problem" manual dispute button is gone (removed August 2024). It's been replaced by AI-driven automated lead credits — and most operators report lead quality has declined since the change. Industry estimates put credit recovery at roughly 6–7% of LSA spend, down from much higher rates under the manual system. As one widely respected local SEO researcher put it, the platform "started filling the leads with a ton of out-of-industry, out-of-city leads."

- As of October 20, 2025, the Google Guaranteed and Google Screened badges were retired and replaced with a single unified blue checkmark "Google Verified" badge. Google's documentation says the badge "appears dynamically when predicted to aid decision-making" — which in practice means it's inconsistently displayed. The visual differentiation that used to set you apart is gone.

- Since November 2024, a linked and verified Google Business Profile is mandatory to run LSAs at all. As of July 2025, all reviews flow through GBP — the separate LSA review system no longer exists. Your GBP is now your LSA's foundation, not a parallel system.

- The "Get Competitive Quotes" feature now sends homeowner messages to up to four top-rated pros simultaneously. Being ranked in the top three LSA spots no longer guarantees you're in the conversation. Response speed is the decisive factor.

- LSA Maps placement is now bundled — you can't opt out of Map placement without pausing Search placement entirely.

Real per-lead costs in early 2026 across major metros:

- HVAC: $45–$80 ($100+ for emergency AC in summer)

- Plumbing: $35–$65

- Electrical: $40–$75

- Roofing: $55–$90 ($150+ during active storm events)

- Garage doors: $25–$40

At a 30% close rate, an $80 HVAC lead is a $267 cost-per-booked-job before tire-kickers, wrong numbers, and price shoppers.

The strategic takeaway: LSAs still work — but they require active management, precise category and geo settings, ruthless response time discipline (sub-30-second answer rates), and an AI-driven lead qualification layer to manage the volume of low-quality leads now flowing through. "Set it and forget it" LSA strategies are quietly bleeding money in 2026. And if LSAs are your only channel, you are one Google algorithm update away from losing 40–60% of your lead volume overnight — operators who built entire businesses on LSAs in 2023–2024 already learned this the hard way.

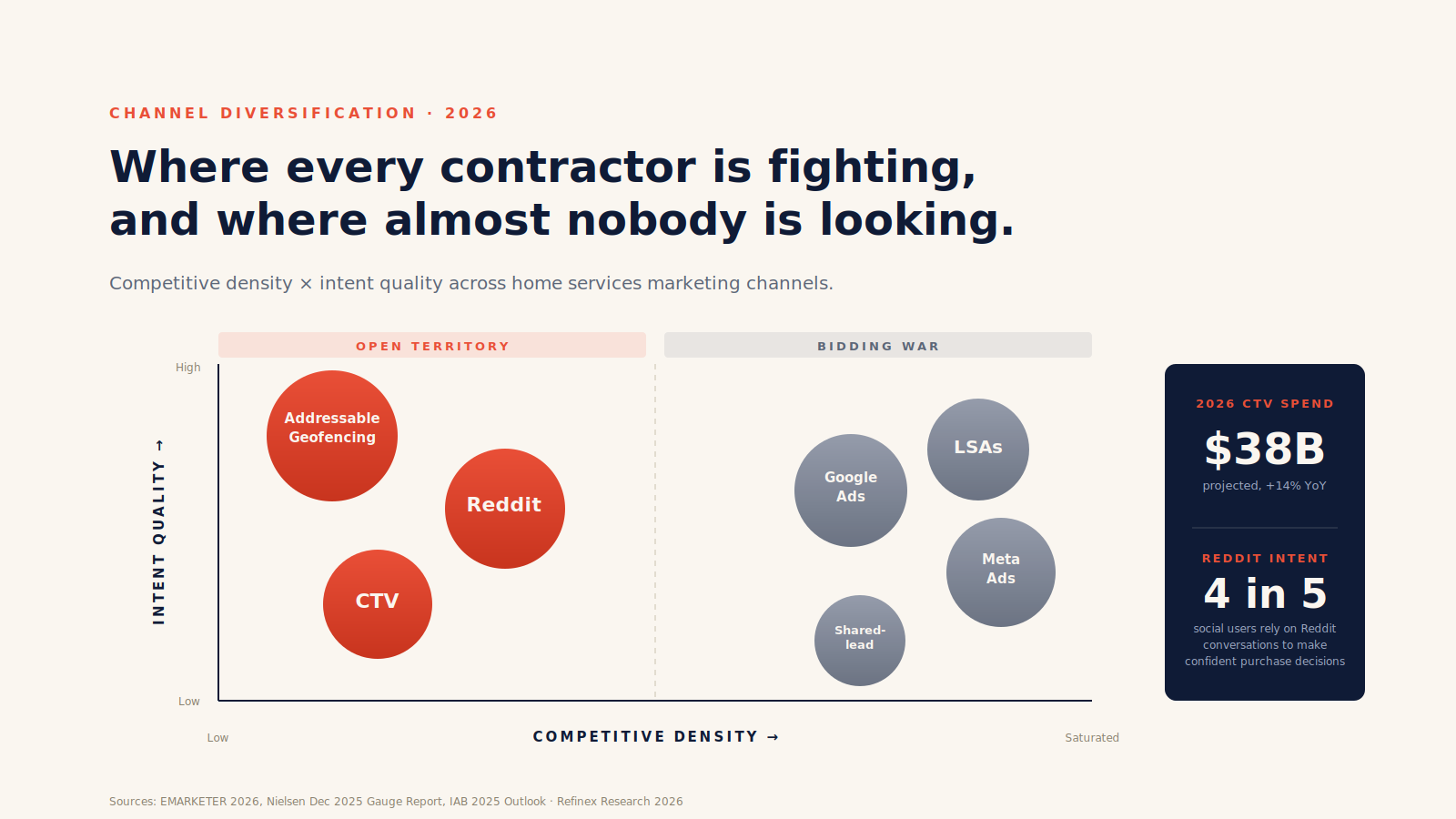

6. Reddit, CTV, and addressable geofencing are the channels your competitors aren't running. That's why they work.

Every home services marketing conversation defaults to the same four channels: Google Ads, LSAs, Facebook/Instagram, and shared-lead platforms. That's where the bidding war is. That's where your CPAs go up every year. And that's where you're shoulder-to-shoulder with everyone else in your zip code.

The interesting work in 2026 is happening on three channels most contractors aren't running.

Reddit — the highest-intent platform almost no contractor is on.

Here's what most home services owners don't know about Reddit:

- 40% of posts on Reddit are commercial in nature — people actively discussing what to buy, who to hire, what worked

- It's the #1 platform where conversations help users make informed product or service decisions (Reddit's own data, corroborated by EMARKETER)

- 4-in-5 social media users rely on Reddit conversations to make confident decisions about products

- The home improvement subreddits (r/HomeImprovement, r/HVAC, r/Plumbing, r/Roofing, regional city subs) are where homeowners discuss kitchen remodels, HVAC quotes, and roofer recommendations in genuine depth

Reddit CPMs and CPCs are dramatically lower than Meta and Google, and competition from home services advertisers is light to nonexistent in most metros. Dynamic Product Ads and full-funnel campaign structures are now live on the platform. Brands like The Home Depot have been early adopters; local contractors mostly haven't woken up to it.

The catch: Reddit punishes advertisers who treat it like Facebook. The platform rewards native, value-led, conversational creative. A generic "best HVAC in Phoenix" ad will get downvoted into oblivion. A genuinely useful post — "what to actually look for when getting a furnace quote," with the brand presence underneath — performs.

Connected TV (CTV) — local-precision streaming, not the TV of 1995.

CTV is no longer cable. U.S. CTV ad spend is projected to hit ~$38 billion in 2026, a 14% YoY jump. Streaming now represents 47.5% of total U.S. TV viewing time (Nielsen, Dec 2025), and roughly 70% of U.S. adults turn to streaming first when watching video. Free Ad-Supported Streaming (FAST) reaches ~60% of U.S. households.

For a contractor, what used to be a $50,000 TV buy is now a $500/month self-serve campaign on Roku Ads Manager or Hulu Ad Manager — with household-level targeting, IP-based geo precision, and proper conversion tracking. CTV ad campaigns can drive 60%+ of attributable conversions in well-instrumented performance datasets despite a smaller impression share, because the screen is the most attention-rich environment in the home.

CTV pairs well with high-ticket trades (roofing replacement, full HVAC system replacement, kitchen/bath remodels) where the homeowner is in a multi-week consideration cycle. The visual showcase of craftsmanship is hard to beat — and the household watching your ad in their living room is doing it on both their TVs, often with both decision-makers present.

Addressable geofencing — the under-the-radar precision tool.

Geofencing has been around for years. Addressable geofencing is different. Instead of throwing a digital fence around a neighborhood, you upload specific property addresses — pulled from plat-line data, property tax records, weather damage maps, age-of-roof data, age-of-HVAC permits, or your own CRM — and deliver ads to every connected device at that physical address: phone, tablet, laptop, smart TV.

Where this gets interesting for home services:

- Roofing after a storm: Hail maps + property data → addressable geofence the affected houses → ads run for ~30 days reinforcing the door-knocker, mailer, and yard signs

- HVAC replacement: Houses with 15+ year old systems (permit data) → addressable campaign with replacement messaging

- Solar/heat pump: Properties matching ICP criteria (income, ownership, age of home, no current solar permit) → addressable + CTV creative

- Neighborhood-of-a-job: While the install truck is parked on a street, addressable-fence the 100 closest houses. They see your brand on every device for the next 4 weeks. That's how single-job neighborhoods turn into five-job neighborhoods.

- B2B target lists (for those selling into property management, GC networks, builders, restoration referral partners): upload the office addresses, run the campaign, follow up with sales outreach that already feels familiar

These three channels share a common trait: they're not where your competitors are looking, which is exactly why they work. Lead costs are lower, attention is higher, and the operators using them well in 2026 are quietly compounding share before anyone else notices.

The strategic takeaway: Diversify off the Google–Meta duopoly while you can still do it cheaply. Every quarter you wait, more contractors discover these channels and CPMs rise.

7. Recurring revenue isn't a "nice-to-have" anymore — it's the multiple-expansion lever PE is paying premium prices for.

Here's something most owners don't think about until they're sitting across from a buyer: memberships and maintenance plans don't just generate extra revenue. They change the valuation math of your entire business.

The reason PE platforms are paying 17–20x EBITDA isn't that home services has changed. It's that recurring-revenue home services platforms have changed. The buyer isn't paying a premium for repair calls. They're paying for predictability — a base of homeowners who pay a monthly or annual fee, who call you first when something breaks, who buy replacement equipment from you instead of the cheapest quote.

A few numbers that crystallize this:

- Increasing customer retention by 5% can lift profits by 25–95% (long-standing HubSpot research, still valid)

- Lifetime value of subscription/membership customers in HVAC and plumbing routinely runs 3–5x that of one-time customers

- 73% of customers cite clear, upfront pricing as a primary reason for choosing a contractor (2026 State of the Trades) — and membership plans are the cleanest way to package transparent pricing

What the best operators are doing in 2026:

- Tiered membership — basic (annual tune-up + priority dispatch + 10% off repairs), premium (twice-yearly + extended warranty + discounted financing), elite (whole-home coverage across HVAC + plumbing + electrical for multi-trade shops)

- Auto-renewal with card-on-file recovery — credit card updaters built into the renewal flow so churn at expiration drops

- Member-only outbound campaigns — when a 15-year-old AC unit is in a member's home, that's a replacement conversation you've earned the right to have

- Cross-sell across trades for multi-service operators — the HVAC member becomes a plumbing customer becomes an electrical panel upgrade

The strategic takeaway: If you ever plan to sell — even a decade from now — every membership signed today compounds your eventual multiple. If you never plan to sell, memberships smooth seasonal revenue, lock out competitors, and turn one-time transactions into 7-year customer relationships. There's no scenario where this is the wrong investment.

8. Consumer trust has fragmented across review platforms, AI, and direct social proof — and the shops winning are running reputation as a system, not a project.

The last shift is about how homeowners actually decide.

The 2026 State of Home Services Marketing Report surfaced a stat that should reset every owner's reputation strategy:

87% of homeowners will not hire a business rated below 4 stars.

67% of business leaders struggle to consistently collect reviews.

Star ratings function as a qualification filter. Below threshold, you don't get to the consideration set. Period. This used to be true for restaurants. In 2026, it's true for the contractor pricing your $25,000 furnace replacement.

But the deeper shift is where trust is being established:

- 83% of homeowners begin their search online — most going to Google first

- 22% now use AI tools (ChatGPT, Perplexity, Gemini) to research vendors or get recommendations — up from a rounding error two years ago

- 56% of homeowners want 24/7 scheduling or after-hours communication

- 78% of contractors use 2+ marketing vendors, and 67% cannot directly connect marketing spend to revenue

That last stat is the punchline. Most home services operators don't actually know which of their channels is working. They have a CRM and a media bill and no clean line connecting the two. So they keep paying for what feels familiar and starve the channels that could compound.

What "reputation as a system" looks like in 2026:

- Review request automation triggered at the right moment in the job lifecycle (immediately after invoice paid, not three weeks later)

- Velocity targets — minimum new reviews per technician per month, tracked on a leaderboard, tied to comp

- Response discipline — every review, positive or negative, responded to within 24 hours, in the owner's voice

- Multi-platform distribution — Google primary, then Yelp, Facebook, BBB, niche industry directories, and forum mentions (which feed AI citations)

- Attribution clarity — UTM tracking, call tracking with source attribution, and a single dashboard that connects ad spend to booked revenue, not just leads

The strategic takeaway: In 2026, "marketing" and "reputation" and "operations" are not three departments. They're one system. The operators who treat them that way — and instrument them properly — pull ahead of competitors who still see them as separate budgets fighting for the same dollar.

So what does this all add up to?

If you scroll back through this and look at the eight forces together, a pattern jumps out.

The home services industry in 2026 is splitting into two groups.

Group A is the operator running on 2020's playbook. Google Ads, LSAs, shared-lead platforms, a Facebook page, a ServiceTitan login, and the same intake process they've had for five years. They're working harder than ever and watching their CPAs climb every quarter. They're losing technicians to PE-backed competitors. They're invisible on AI search. They have no membership base. They can't tell you which channel made them money last month.

Group B is the operator who has done the boring, expensive work of engineering their business as a system: AI-driven speed-to-lead and intake, full-stack attribution, channel diversification into Reddit/CTV/geofencing, a real membership program, content and reviews built to be cited by AI engines, and a back-office that converts at 2–3x the industry average.

Group B is smaller. Group B is winning. And the gap between the two is widening every quarter.

The good news: nothing in this article requires you to be Apex Service Partners to execute. It requires precision, the right partner stack, and the discipline to actually ship the boring infrastructure work most owners skip.

A note on who wrote this — and why

This article was put together by Dillon Johnson at Refinex — a paid media and AI-driven lead generation agency built specifically for home services and B2B operators. We run the geofencing campaigns. We build the AI voice and SMS speed-to-lead infrastructure. We run the Reddit, CTV, and addressable programs. We instrument the attribution. We do the unglamorous integration work that makes all eight of these trends actually move revenue inside a contractor's P&L.

If something in this article gave you a "we're not doing that yet — and we should be" moment, that's the conversation Dillon loves to have.

You can book a no-pressure 30-minute strategy call with Dillon at Book Dillon. We'll look at your current channels, your speed-to-lead, your attribution gaps, and give you a candid read on where you're leaking money — whether you work with us or not.

The contractors who get ahead of these shifts in 2026 will own their markets through 2028 and beyond. The map is on the wall. The window to move is open. Now is a very good time to move.

Refinex Ad Solutions / RefinexMedia Inc. — Toronto, ON. We build paid media, AI voice & SMS follow-up, programmatic geofencing, and full-funnel attribution systems for home services and B2B companies in North America.

If you run a home services company in 2026, you're operating in the most lucrative — and most violently restructuring — version of this industry that's ever existed. The U.S. home services market is sitting between $650B and $750B annually. Demand is durable. In some trades, margins are the best they've ever been. And yet a lot of owners we talk to feel like the ground is moving under them.

It is.

What follows isn't a list of buzzwords or "tips to optimize your Google Business Profile." It's eight specific, well-documented shifts reshaping how money, leads, labor, and ownership flow through this industry — and what each one means for the operator who has to make payroll on Friday. The research behind this is pulled from PE deal trackers, SEC filings, BLS data, Google's own product documentation, the 2026 State of the Trades survey of 1,000+ contractors, Scorpion's 2026 survey of 2,000 homeowners, Whitespark's Q2 2026 local data set, and a stack of primary platform research most owners will never have time to read.

Read it through once. There's a payoff at the end.

In this guide

- Private equity isn't coming. It already came.

- The skilled labor shortage is a margin problem in disguise

- AI voice and SMS follow-up: from experiment to table stakes

- Google search just changed under you

- Google LSAs got harder, more expensive, structurally different

- Reddit, CTV, and addressable geofencing

- Recurring revenue is now a multiple-expansion lever

- Consumer trust has fragmented across platforms

- So what does this all add up to?

- A note on who wrote this — and why

1. Private equity isn't coming. It already came. And it's the single biggest force in your market right now.

Let's start with the shift that's restructuring the industry beneath everyone's feet.

In 2025, Blackstone agreed to pay roughly $2.5 billion for Champions Group, a residential HVAC, plumbing, and electrical platform — at an implied multiple of around 18.5x EBITDA. A few months earlier, Goldman Sachs Alternatives took a majority stake in Sila Services at a reported $1.7 billion valuation, in the 17–20x range. Apex Service Partners alone closed roughly 60 add-on acquisitions in 2025 — more than the entire publicly tracked plumbing roll-up cohort combined.

The numbers behind the headlines:

- PE add-on activity in home services rose 88% year-over-year through mid-2025

- Strategic buyers now account for ~80% of all HVAC service transactions

- At least 27 active PE-backed platforms are competing for the same fragmented owner pool, with over $50B+ in committed capital

- Apex alone has raised over $6 billion in funding, including a $3.4B continuation fund — a structural signal that this is a multi-decade hold, not a 3–5 year flip

This is not a fad. It is a permanent restructuring of the competitive landscape. And it matters whether you want to sell or not.

Why this affects you even if you'd never sell in a million years:

When a PE-backed platform buys a competitor in your service area, three things happen within 12 months. First, they centralize back-office, get supply-house discounts you can't match, and squeeze 4–6 points of margin out of operations. Second, they raise technician pay — Alpine Investors reports a 20% average technician pay bump in year one post-acquisition — which pulls your best people. Third, they deploy a marketing budget calibrated against a portfolio of brands, not a single P&L, and they can run at a loss on lead acquisition in your market for 18 months to take share.

A huge tell most owners miss: many of these PE-owned shops keep the same local name, same family-feel branding, same logo after acquisition. The neighborhood doesn't know anything changed. But behind the scenes, the cost structure, the marketing budget, and the playbook just got an enterprise upgrade.

The strategic takeaway: The independent operator who isn't actively countering this is, quietly, losing a race they don't know they're running. The counter-move isn't to outspend them. It's to out-precision them: own a tighter ICP, run faster speed-to-lead, build channels they can't bolt on with a checkbook.

2. The skilled labor shortage isn't a hiring problem. It's a margin problem in disguise.

Every owner reading this already knows the labor side of the story:

- The U.S. construction industry is short ~530,000 workers in 2026

- For every 3 tradespeople retiring, only 1 new worker enters the field (NCCER)

- Projected 2026 shortages: 20,000+ licensed plumbers and nearly 40,000 HVAC technicians in the U.S. alone

- Median age of plumbers and HVAC techs now exceeds 40

Here's the part most operators are still underestimating: the labor shortage isn't your biggest bottleneck. Your back office is.

The single most consistent insight from operators running $5M–$50M shops right now is that field talent is half the battle. The other half — dispatch, intake, follow-up, estimate-to-close, scheduling, billing — is where deals die quietly. You can hire two more techs. But if they sit idle because intake isn't converting, or because nobody followed up on the 47 leads from last month, the new hires don't fix anything.

The math is brutal and worth sitting with:

A 2-tech shop missing 2 booked jobs per week at a $500 average ticket loses $52,000 a year. A 6-tech shop missing 8 booked jobs per week at $1,200 average ticket loses ~$500,000 a year.

Most owners don't measure this because the missed jobs never enter a CRM. They were a missed call, a slow text-back, a quote that didn't get followed up on day 3.

The strategic takeaway: The winning operators in 2026 aren't the ones with the most techs. They're the ones whose office-side conversion is engineered as carefully as their field operations. Speed-to-lead, follow-up cadence, and intake quality are now the highest-leverage margin levers in this industry — and most owners are still under-investing in them by an order of magnitude.

3. AI voice and SMS follow-up moved from "experiment" to "table stakes" in 18 months. Quietly.

You've heard the noise about AI. Strip away the hype and look at what's actually shipping into production at well-run shops.

The behavioral data that matters:

- Up to 78% of leads go to the first business that responds (HBR's foundational research on speed-to-lead, now widely confirmed)

- A lead responded to in 5 minutes vs. 30 minutes is 21x more likely to qualify

- The shared-lead platforms most contractors complain about (you know the names) sell the same homeowner to 3–5 contractors. First responder wins. Everyone else paid for nothing.

- Nearly 60% of homeowners who call after-hours and don't get a live answer will not call back

- HVAC contractors deploying always-on AI voice routinely report 40–50% increases in booked appointments from after-hours alone

In 2024, voice AI in home services was a curiosity. In Q1 2026, it is a settled question. A 2026 industry survey of contractors found about 25% are using AI meaningfully today — meaning roughly three-quarters of the market hasn't adopted yet. That gap is the opportunity. By the time penetration crosses 50%, voice AI stops being an advantage and starts being table stakes. Industry analysts project that crossover happens by end of 2026.

What good AI implementation actually looks like in this trade (not the demo-ware version):

- Inbound voice agents that answer in two rings, qualify on the call, hand off urgency to a human, and write the appointment into the calendar — not "press 1 for service"

- Outbound speed-to-lead that calls a web lead within 60 seconds of submission, before the homeowner has even closed the tab

- SMS follow-up sequences that pursue the 40% of leads who said "let me think about it" — most shops abandon these by day 2; a disciplined sequence over 14 days recovers a measurable share

- Multilingual handling — Spanish-speaking callers handled natively, no transfer drop-off

The catch most owners miss: voice AI is only as good as the systems plumbing behind it. If the AI books an appointment but doesn't sync to your dispatch, doesn't tag the lead source, doesn't enrich the contact with property data, doesn't trigger a follow-up if the homeowner ghosts — you've bought a fancy answering service. The competitive edge is in the integration, not the voice model.

The strategic takeaway: Speed-to-lead under 60 seconds, 24/7, with intelligent qualification, is the single largest lift available to most home services operators right now. It's also the single biggest gap between the top quartile and everyone else. The shops that lock this down in 2026 will be impossible to compete with on lead economics in 2027.

4. Google search just changed under you — and most contractors haven't noticed yet.

This one is the silent killer of 2026, and it's the trend that's least talked about because most contractors don't read SEO research.

A 2026 local SEO data set found that AI Overviews now appear on 68% of local searches, 92% of informational local queries, and 97% of hybrid-intent queries like "average cost of HVAC replacement in Calgary." Map packs — the three-pack contractors fought for in the 2010s — now only appear on 39% of local searches.

Translate that:

The spot at the top of Google that you've been competing for, with your reviews and your GBP, no longer exists on most of the searches your customers are running.

What replaced it is a synthesized AI answer that names one to three businesses in your metro by name. Across all local business listings, only about 1.2% get cited by AI search engines (SOCi 2026 Local Visibility Index). For local services categories, only 15% of cited businesses capture the top recommendation slot where the actual conversion happens.

And the consumer behavior shift driving this is happening faster than most owners realize:

- 41% of consumers now trust AI recommendations for local services "as much or more" than personal referrals — up from 12% in 2024

- 1 in 3 homeowners under 45 have used an AI assistant to find a home service provider in the past 90 days

- AI-referred leads convert at substantially higher rates than Google organic leads because the homeowner already trusts the AI's recommendation before the call

This isn't theoretical. It's already how a meaningful slice of your customer base is finding their next contractor. And the contractors who get cited now will compound that authority: every AI-referred customer leaves a review, the review strengthens the trust signal, the AI cites them more often. The map-pack winner-take-most dynamic of the 2010s is repeating itself in AI search, and the lock-in is happening through 2026.

What actually moves the needle on AI citation (different from traditional SEO):

- Multi-source consensus — your business mentioned consistently across GBP, niche directories, forums (Reddit included), local news, industry publications — not just on your own site

- Structured data done correctly — proper LocalBusiness, Service, and FAQ schema. Sites with FAQ schema are 2.8x more likely to be cited in AI answers (FogLift 2026 study).

- Content that directly answers high-intent questions — "how do I know if my furnace is failing," "what does a tankless install cost in [city]," "how long do heat pumps last" — written like a tradesperson actually answers them, not like an SEO content mill

- Freshness — pages not refreshed quarterly are 3x more likely to lose AI citations than recently updated pages (AirOps research)

- Review velocity, not just volume — recent reviews matter more than historical totals

The strategic takeaway: If your entire local search strategy is "rank in the map pack and run LSAs," you are optimizing for a surface area that is shrinking every month. The contractors who own the AI citation in their metro by mid-2026 will own the recommendation slot through 2028, the same way map-pack winners owned the 2010s. Most of your competitors are still asleep on this. That's the window.

5. Google Local Service Ads got harder, more expensive, and structurally different — and the playbook from 2023 is actively losing money in 2026.

LSAs are still one of the highest-ROI channels in home services. They're also a very different product than they were 18 months ago, and a lot of owners are running them on autopilot with last year's strategy.

The structural changes you need to know:

- The old "Report a Problem" manual dispute button is gone (removed August 2024). It's been replaced by AI-driven automated lead credits — and most operators report lead quality has declined since the change. Industry estimates put credit recovery at roughly 6–7% of LSA spend, down from much higher rates under the manual system. As one widely respected local SEO researcher put it, the platform "started filling the leads with a ton of out-of-industry, out-of-city leads."

- As of October 20, 2025, the Google Guaranteed and Google Screened badges were retired and replaced with a single unified blue checkmark "Google Verified" badge. Google's documentation says the badge "appears dynamically when predicted to aid decision-making" — which in practice means it's inconsistently displayed. The visual differentiation that used to set you apart is gone.

- Since November 2024, a linked and verified Google Business Profile is mandatory to run LSAs at all. As of July 2025, all reviews flow through GBP — the separate LSA review system no longer exists. Your GBP is now your LSA's foundation, not a parallel system.

- The "Get Competitive Quotes" feature now sends homeowner messages to up to four top-rated pros simultaneously. Being ranked in the top three LSA spots no longer guarantees you're in the conversation. Response speed is the decisive factor.

- LSA Maps placement is now bundled — you can't opt out of Map placement without pausing Search placement entirely.

Real per-lead costs in early 2026 across major metros:

- HVAC: $45–$80 ($100+ for emergency AC in summer)

- Plumbing: $35–$65

- Electrical: $40–$75

- Roofing: $55–$90 ($150+ during active storm events)

- Garage doors: $25–$40

At a 30% close rate, an $80 HVAC lead is a $267 cost-per-booked-job before tire-kickers, wrong numbers, and price shoppers.

The strategic takeaway: LSAs still work — but they require active management, precise category and geo settings, ruthless response time discipline (sub-30-second answer rates), and an AI-driven lead qualification layer to manage the volume of low-quality leads now flowing through. "Set it and forget it" LSA strategies are quietly bleeding money in 2026. And if LSAs are your only channel, you are one Google algorithm update away from losing 40–60% of your lead volume overnight — operators who built entire businesses on LSAs in 2023–2024 already learned this the hard way.

6. Reddit, CTV, and addressable geofencing are the channels your competitors aren't running. That's why they work.

Every home services marketing conversation defaults to the same four channels: Google Ads, LSAs, Facebook/Instagram, and shared-lead platforms. That's where the bidding war is. That's where your CPAs go up every year. And that's where you're shoulder-to-shoulder with everyone else in your zip code.

The interesting work in 2026 is happening on three channels most contractors aren't running.

Reddit — the highest-intent platform almost no contractor is on.

Here's what most home services owners don't know about Reddit:

- 40% of posts on Reddit are commercial in nature — people actively discussing what to buy, who to hire, what worked

- It's the #1 platform where conversations help users make informed product or service decisions (Reddit's own data, corroborated by EMARKETER)

- 4-in-5 social media users rely on Reddit conversations to make confident decisions about products

- The home improvement subreddits (r/HomeImprovement, r/HVAC, r/Plumbing, r/Roofing, regional city subs) are where homeowners discuss kitchen remodels, HVAC quotes, and roofer recommendations in genuine depth

Reddit CPMs and CPCs are dramatically lower than Meta and Google, and competition from home services advertisers is light to nonexistent in most metros. Dynamic Product Ads and full-funnel campaign structures are now live on the platform. Brands like The Home Depot have been early adopters; local contractors mostly haven't woken up to it.

The catch: Reddit punishes advertisers who treat it like Facebook. The platform rewards native, value-led, conversational creative. A generic "best HVAC in Phoenix" ad will get downvoted into oblivion. A genuinely useful post — "what to actually look for when getting a furnace quote," with the brand presence underneath — performs.

Connected TV (CTV) — local-precision streaming, not the TV of 1995.

CTV is no longer cable. U.S. CTV ad spend is projected to hit ~$38 billion in 2026, a 14% YoY jump. Streaming now represents 47.5% of total U.S. TV viewing time (Nielsen, Dec 2025), and roughly 70% of U.S. adults turn to streaming first when watching video. Free Ad-Supported Streaming (FAST) reaches ~60% of U.S. households.

For a contractor, what used to be a $50,000 TV buy is now a $500/month self-serve campaign on Roku Ads Manager or Hulu Ad Manager — with household-level targeting, IP-based geo precision, and proper conversion tracking. CTV ad campaigns can drive 60%+ of attributable conversions in well-instrumented performance datasets despite a smaller impression share, because the screen is the most attention-rich environment in the home.

CTV pairs well with high-ticket trades (roofing replacement, full HVAC system replacement, kitchen/bath remodels) where the homeowner is in a multi-week consideration cycle. The visual showcase of craftsmanship is hard to beat — and the household watching your ad in their living room is doing it on both their TVs, often with both decision-makers present.

Addressable geofencing — the under-the-radar precision tool.

Geofencing has been around for years. Addressable geofencing is different. Instead of throwing a digital fence around a neighborhood, you upload specific property addresses — pulled from plat-line data, property tax records, weather damage maps, age-of-roof data, age-of-HVAC permits, or your own CRM — and deliver ads to every connected device at that physical address: phone, tablet, laptop, smart TV.

Where this gets interesting for home services:

- Roofing after a storm: Hail maps + property data → addressable geofence the affected houses → ads run for ~30 days reinforcing the door-knocker, mailer, and yard signs

- HVAC replacement: Houses with 15+ year old systems (permit data) → addressable campaign with replacement messaging

- Solar/heat pump: Properties matching ICP criteria (income, ownership, age of home, no current solar permit) → addressable + CTV creative

- Neighborhood-of-a-job: While the install truck is parked on a street, addressable-fence the 100 closest houses. They see your brand on every device for the next 4 weeks. That's how single-job neighborhoods turn into five-job neighborhoods.

- B2B target lists (for those selling into property management, GC networks, builders, restoration referral partners): upload the office addresses, run the campaign, follow up with sales outreach that already feels familiar

These three channels share a common trait: they're not where your competitors are looking, which is exactly why they work. Lead costs are lower, attention is higher, and the operators using them well in 2026 are quietly compounding share before anyone else notices.

The strategic takeaway: Diversify off the Google–Meta duopoly while you can still do it cheaply. Every quarter you wait, more contractors discover these channels and CPMs rise.

7. Recurring revenue isn't a "nice-to-have" anymore — it's the multiple-expansion lever PE is paying premium prices for.

Here's something most owners don't think about until they're sitting across from a buyer: memberships and maintenance plans don't just generate extra revenue. They change the valuation math of your entire business.

The reason PE platforms are paying 17–20x EBITDA isn't that home services has changed. It's that recurring-revenue home services platforms have changed. The buyer isn't paying a premium for repair calls. They're paying for predictability — a base of homeowners who pay a monthly or annual fee, who call you first when something breaks, who buy replacement equipment from you instead of the cheapest quote.

A few numbers that crystallize this:

- Increasing customer retention by 5% can lift profits by 25–95% (long-standing HubSpot research, still valid)

- Lifetime value of subscription/membership customers in HVAC and plumbing routinely runs 3–5x that of one-time customers

- 73% of customers cite clear, upfront pricing as a primary reason for choosing a contractor (2026 State of the Trades) — and membership plans are the cleanest way to package transparent pricing

What the best operators are doing in 2026:

- Tiered membership — basic (annual tune-up + priority dispatch + 10% off repairs), premium (twice-yearly + extended warranty + discounted financing), elite (whole-home coverage across HVAC + plumbing + electrical for multi-trade shops)

- Auto-renewal with card-on-file recovery — credit card updaters built into the renewal flow so churn at expiration drops

- Member-only outbound campaigns — when a 15-year-old AC unit is in a member's home, that's a replacement conversation you've earned the right to have

- Cross-sell across trades for multi-service operators — the HVAC member becomes a plumbing customer becomes an electrical panel upgrade

The strategic takeaway: If you ever plan to sell — even a decade from now — every membership signed today compounds your eventual multiple. If you never plan to sell, memberships smooth seasonal revenue, lock out competitors, and turn one-time transactions into 7-year customer relationships. There's no scenario where this is the wrong investment.

8. Consumer trust has fragmented across review platforms, AI, and direct social proof — and the shops winning are running reputation as a system, not a project.

The last shift is about how homeowners actually decide.

The 2026 State of Home Services Marketing Report surfaced a stat that should reset every owner's reputation strategy:

87% of homeowners will not hire a business rated below 4 stars.

67% of business leaders struggle to consistently collect reviews.

Star ratings function as a qualification filter. Below threshold, you don't get to the consideration set. Period. This used to be true for restaurants. In 2026, it's true for the contractor pricing your $25,000 furnace replacement.

But the deeper shift is where trust is being established:

- 83% of homeowners begin their search online — most going to Google first

- 22% now use AI tools (ChatGPT, Perplexity, Gemini) to research vendors or get recommendations — up from a rounding error two years ago

- 56% of homeowners want 24/7 scheduling or after-hours communication

- 78% of contractors use 2+ marketing vendors, and 67% cannot directly connect marketing spend to revenue

That last stat is the punchline. Most home services operators don't actually know which of their channels is working. They have a CRM and a media bill and no clean line connecting the two. So they keep paying for what feels familiar and starve the channels that could compound.

What "reputation as a system" looks like in 2026:

- Review request automation triggered at the right moment in the job lifecycle (immediately after invoice paid, not three weeks later)

- Velocity targets — minimum new reviews per technician per month, tracked on a leaderboard, tied to comp

- Response discipline — every review, positive or negative, responded to within 24 hours, in the owner's voice

- Multi-platform distribution — Google primary, then Yelp, Facebook, BBB, niche industry directories, and forum mentions (which feed AI citations)

- Attribution clarity — UTM tracking, call tracking with source attribution, and a single dashboard that connects ad spend to booked revenue, not just leads

The strategic takeaway: In 2026, "marketing" and "reputation" and "operations" are not three departments. They're one system. The operators who treat them that way — and instrument them properly — pull ahead of competitors who still see them as separate budgets fighting for the same dollar.

So what does this all add up to?

If you scroll back through this and look at the eight forces together, a pattern jumps out.

The home services industry in 2026 is splitting into two groups.

Group A is the operator running on 2020's playbook. Google Ads, LSAs, shared-lead platforms, a Facebook page, a ServiceTitan login, and the same intake process they've had for five years. They're working harder than ever and watching their CPAs climb every quarter. They're losing technicians to PE-backed competitors. They're invisible on AI search. They have no membership base. They can't tell you which channel made them money last month.

Group B is the operator who has done the boring, expensive work of engineering their business as a system: AI-driven speed-to-lead and intake, full-stack attribution, channel diversification into Reddit/CTV/geofencing, a real membership program, content and reviews built to be cited by AI engines, and a back-office that converts at 2–3x the industry average.

Group B is smaller. Group B is winning. And the gap between the two is widening every quarter.

The good news: nothing in this article requires you to be Apex Service Partners to execute. It requires precision, the right partner stack, and the discipline to actually ship the boring infrastructure work most owners skip.

A note on who wrote this — and why

This article was put together by Dillon Johnson at Refinex — a paid media and AI-driven lead generation agency built specifically for home services and B2B operators. We run the geofencing campaigns. We build the AI voice and SMS speed-to-lead infrastructure. We run the Reddit, CTV, and addressable programs. We instrument the attribution. We do the unglamorous integration work that makes all eight of these trends actually move revenue inside a contractor's P&L.

If something in this article gave you a "we're not doing that yet — and we should be" moment, that's the conversation Dillon loves to have.

You can book a no-pressure 30-minute strategy call with Dillon at Book Dillon. We'll look at your current channels, your speed-to-lead, your attribution gaps, and give you a candid read on where you're leaking money — whether you work with us or not.

The contractors who get ahead of these shifts in 2026 will own their markets through 2028 and beyond. The map is on the wall. The window to move is open. Now is a very good time to move.

Refinex Ad Solutions / RefinexMedia Inc. — Toronto, ON. We build paid media, AI voice & SMS follow-up, programmatic geofencing, and full-funnel attribution systems for home services and B2B companies in North America.